This first Family Business Pulse survey presents a mixed picture of the current operating environment for UK family businesses.

While changes to BPR and APR have weighed on employment and investment intentions, the data also show that family businesses remain committed to job creation. However, the conditions in which they operate must be supportive and tailored to their needs.

Family businesses are eager to grow employment, but increasing cost pressures and geopolitical uncertainty are slowing the pace more than they would ideally like.

A renewed focus on reducing the burden of National Insurance Contributions, alongside careful management of the National Minimum Wage and National Living Wage, will be essential.

Equally important is the effective implementation of Employment Rights reforms, underpinned by full and meaningful consultation. These measures will help create an environment in which family businesses can feel more confident about creating new jobs. In parallel, stronger fiscal incentives are needed to support young people into work – particularly given the persistently high unemployment rates among 16–24-year-olds.

To unlock investment and growth, the UK needs a tax environment that supports the sector’s untapped potential. With the Budget just five months away, government must respond to the priorities highlighted in our survey, most notably delivering comprehensive business rates reform and simplifying the wider tax system.

Although businesses report strong confidence in their own growth prospects, this is tempered by significantly lower confidence in the broader UK economic outlook. Bridging this gap is critical.

Greater certainty will not only support investment decisions but also underpin effective succession planning and the development of the next generation of leadership. The Family Business Pulse highlights a growing need for enhanced leadership and management development within family firms, to support succession planning and the future health of the sector. FBUK is calling on government to expand Help to Grow1, with a stronger focus on succession in family businesses.

1www.gov.uk/business-finance-support/help-to-grow-management-uk

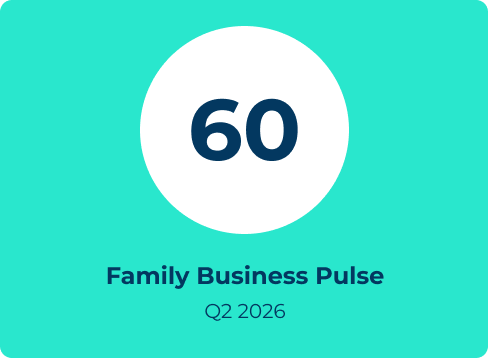

Family business ‘Pulse’ score

The first quarterly Family Business Pulse shows a score of 60 out of 100 –

demonstrating medium levels of confidence.

This Pulse score is based on four index questions, each aligned to a core pillar

of Family Business UK’s work. Each question is weighted equally at 25 points,

creating a total index score out of 100.

To support analysis, we group results into three categories (low, medium

and high confidence) to enable comparison across performance levels and

highlight key behavioural differences.

Scoring system

50 or less

Low confidence

51-65

Medium confidence

66+

High confidence

The index covers four key areas: i) family ownership and succession; ii) business performance and confidence; iii) investment, growth and innovation iv) confidence in the economy. Each area contributes up to 25 points to the overall score.

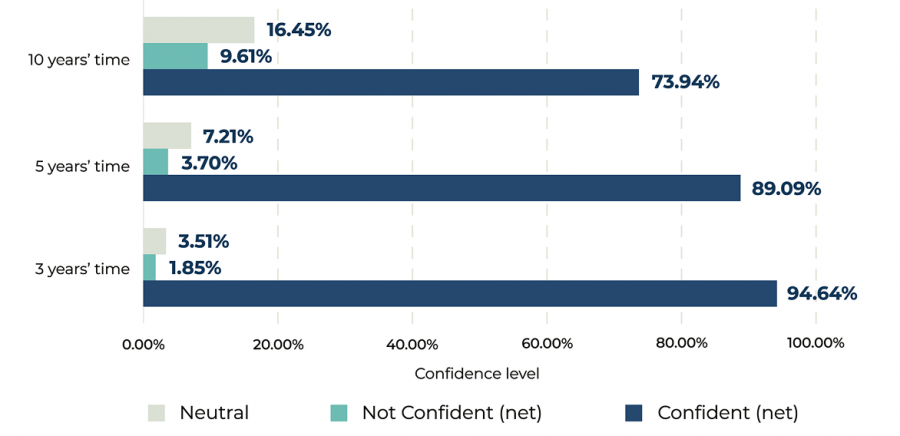

Family business confidence

Looking specifically at family ownership, confidence remains high in the short term: 95% of respondents believe their business will still be family-owned in three years’ time. This confidence declines over the longer term, falling to 74% who expect the business to remain family-owned in ten years.

Business owners in the retail, hospitality and leisure sectors reported lower confidence in remaining family-owned over the next ten years, with 68% expressing confidence.

How confident, if at all, are you that your business will remain family-owned over the next 3, 5 and 10 years?

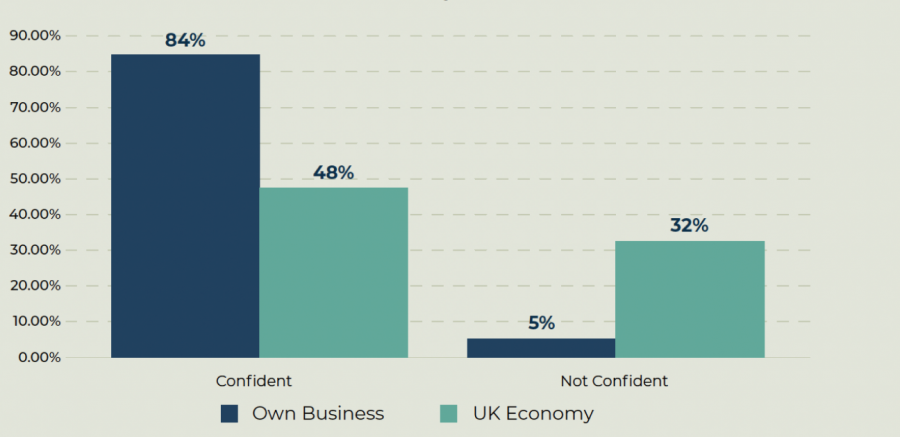

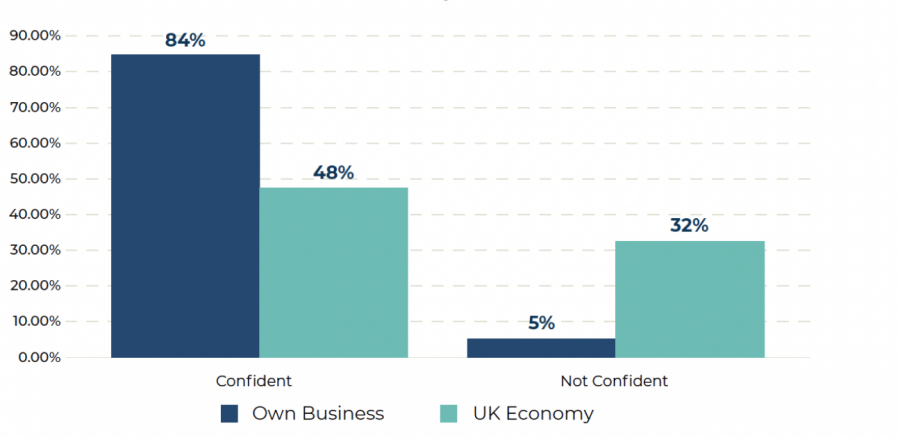

Growth prospects

Family business owners demonstrate a strong sense of confidence in the

future growth of their own organisations. However, confidence in wider UK

economic growth is more mixed, with fewer than half expressing optimism

about future prospects.

88% of medium-sized family businesses said they were confident in their

prospects over the next 12 months, compared to 80% of small businesses.

In addition, 60% of businesses in London said they were confident in the

growth of the UK economy, compared to 41% in the North-West.

How confident are you about the growth prospects of your business and the UK economy over the next 12 months?

Business sales

Our survey showed that more than two thirds (68%) of family businesses trade internationally. Among those family businesses that do trade internationally nearly a third (31%) reported an increase in their international sales over the last quarter, while only 9% experienced a decline.

In terms of domestic sales, half of family businesses (50%) say sales were higher than forecast. West Midlands based family businesses recorded the highest increase in sales with 56% of firms reporting increases (18%, increasing significantly and 36% increasing slightly).

How did your sales perform over the last quarter against your predicted forecasts?

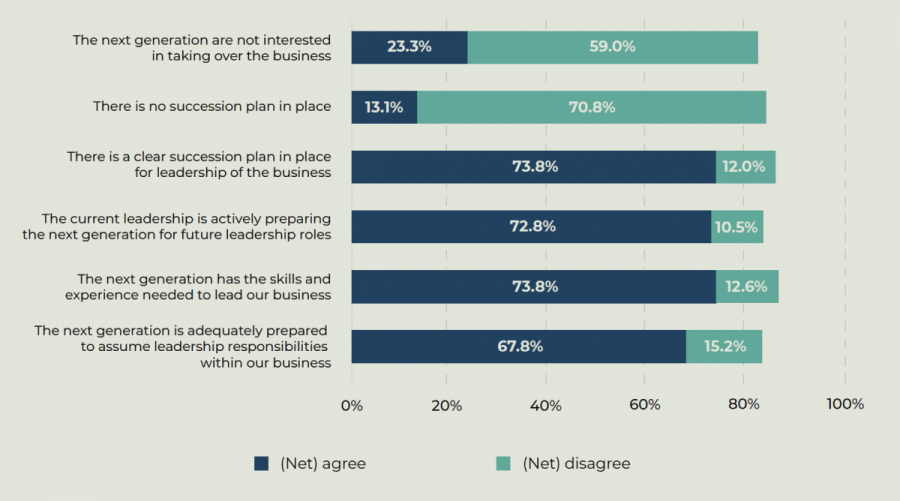

Business succession

The Family Business Pulse shows that while Britain’s family-owned businesses often have clear succession plans in place, preparedness for leadership transition is less assured.

Although three quarters (74%) of family businesses believe the next generation has the necessary skills and experience, a smaller proportion (68%) believe the next generation is adequately prepared to take on leadership responsibilities.

To what extent do you agree or disagree with the following statements about leadership succession in your family business?

Tax factors

The three tax factors currently having the greatest impact on family businesses are Employer National Insurance Contributions (32%), business rates (29%), the National Minimum Wage / National Living Wage (28%).

Looking ahead, the types of tax support that family business owners say would most support investment and growth in their business over the next 12 months include reducing Employer NICs (38%), business rates reform (37%), VAT simplification (31%). 56% of businesses that have been operating for over 40 years said that employer NICs were having the greatest impact on their business.

Almost four in ten (38%) medium and large family businesses

said the future growth of their business would be supported by

reforming new Inheritance Tax rules introduced on 6 April.

BPR / APR

Since changes to BPR / APR were announced, Family businesses have invested significantly in legal and financial advice. Nevertheless, more than half of family firms (51%) still expect to be affected by the changes.

Medium and large family businesses remain the most exposed: 62% of those employing more than 50 people say they will be affected by the changes.

The changes to BPR / APR have continue to impact jobs and investment. 18% of family businesses have deferred or reduced investment over the last 12 months while 17% have cut jobs or frozen recruitment.

These trends look set to continue. Over the next 12 months, 16% of family firms plan to reduce headcount or freeze recruitment, and around 14% expect to defer, pause, or cancel investment.

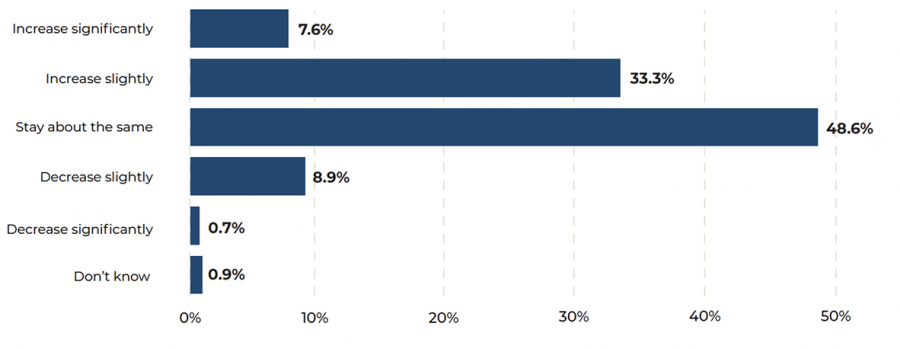

Employment intentions

Family businesses remain broadly optimistic about employment over the next 12 months, with 41% expecting to increase their workforce however this has been reduced due to increasing costs and uncertainty. Expectations for employment growth are strongest in the sales, media & marketing, IT and telecoms, and architecture, engineering & building sectors.

Alongside geopolitical uncertainties, family businesses face several barriers to hiring. The most significant challenges are high wage expectations (40%), rising employment costs (37%), a lack of candidates with the right skills (25%), uncertainty about future demand (24%).

Rising employment costs are a particular concern in certain sectors with almost half (48%) of businesses in retail, hospitality, and leisure citing this as the biggest barrier to recruiting staff.

Over the next 12 months, to what extent do you expect to increase or decrease the number of people you directly employ in your business?

Access to finance

Over the past year, family businesses found internal sources of finance, such as retained earnings and owner capital, easier to access than external funding options, including debt finance (e.g. loans and credit lines) and equity investment from external investors.

Over the past 12 months, how easy or hard did you find it for your family business to access finance?

| Funding source | Easy (Net) | Hard (Net) | Neutral | N/A |

|---|---|---|---|---|

| Internal funding | 41.77% | 8.5% | 31.42% | 18.3% |

| Debt financing | 37.15% | 11.46% | 25.69% | 25.69% |

| Equity financing | 31.98% | 9.24% | 26.25% | 32.53% |

| Government grants | 27.36% | 19.59% | 22.37% | 30.68% |

| Other forms of finance | 24.4% | 8.32% | 28.28% | 39% |

Geopolitical conditions

As a result of recent geopolitical tensions in the Middle East, more than four in ten family businesses (43%) report being affected by rising costs, including increases in raw materials, shipping, and insurance. Among those impacted, around a third (34%) say costs have risen by between 10% and 19%, while a similar proportion (31%) have experienced increases of between 20% and 39%.

Among family businesses experiencing rising costs, a significant proportion are passing on those increases to customers. More than a third (37%) of family businesses say they have adjusted pricing to reflect higher input costs.

However, the fallout of the conflict extends beyond jobs and prices. Family businesses are also reporting significant impacts in disruption to supply chains, lower customer demand in key markets, difficulty accessing international markets and increased finance costs. Almost one quarter (24%) of family firms say uncertainty has hit their ability to make long-term plans, a key trait of family ownership, while more than one in five (22%) say they have been forced to reduce or postpone planned business investment as a result of the conflict.